Debt can feel overwhelming — especially when you’re juggling credit cards, personal loans, BNPL balances, or student loans. But one of the most powerful, psychology-backed repayment strategies is the debt snowball method.

Now, with modern fintech budgeting apps, AI-powered money trackers, and automated payment tools, you can implement a debt snowball plan faster and more efficiently than ever.

This step-by-step guide will show you how to:

✔ Build a debt snowball using fintech apps

✔ Automate payments and track progress

✔ Stay motivated with visual payoff milestones

✔ Reduce interest and eliminate debt faster

If you want a structured, tech-powered debt payoff system, this is your complete roadmap.

What Is the Debt Snowball Method?

The debt snowball strategy focuses on paying off debts from smallest balance to largest, regardless of interest rate.

Here’s how it works:

- List all debts from smallest to largest balance

- Pay minimum payments on all debts

- Put extra money toward the smallest debt

- Once paid off, roll that payment into the next debt

This creates momentum — like a snowball rolling downhill.

Why Use Fintech Apps for a Debt Snowball?

Modern fintech tools make the process:

✔ Automated

✔ Visual

✔ Data-driven

✔ Motivational

Instead of spreadsheets, you get:

- Real-time balance tracking

- Payment reminders

- AI cash flow insights

- Goal progress dashboards

Step 1: List All Your Debts in a Fintech App

Start by entering:

- Credit cards

- Personal loans

- Buy now pay later balances

- Student loans

- Overdrafts

Most budgeting apps auto-sync balances from your bank.

Key Data to Include

✔ Balance

✔ Minimum payment

✔ Interest rate

✔ Due date

Step 2: Sort Debts by Balance (Not Interest Rate)

The snowball method prioritizes quick wins.

Example:

| Debt | Balance | Minimum Payment |

|---|---|---|

| Credit Card A | $300 | $25 |

| BNPL Balance | $600 | $50 |

| Personal Loan | $2,000 | $120 |

| Credit Card B | $4,500 | $180 |

You’ll attack Credit Card A first, even if its interest is lower.

Step 3: Set Your Extra Payment Amount

Open your fintech budgeting dashboard and calculate:

Monthly income – expenses = extra debt payment

Even $50–$100 extra per month accelerates payoff.

Many apps now offer:

✔ AI spending analysis

✔ Subscription cancellation suggestions

✔ Smart savings transfers

Use these to free up extra cash.

Step 4: Automate Minimum Payments

Automation prevents:

❌ Late fees

❌ Credit score damage

Set auto-pay for minimums on all debts.

Then manually direct your extra payment to the smallest balance.

Step 5: Use Visual Progress Trackers

Fintech apps often include:

- Debt payoff charts

- Goal progress bars

- Estimated payoff dates

These increase motivation and consistency.

Psychology matters — seeing a balance hit $0 builds momentum.

Step 6: Roll Payments Forward (The Snowball Effect)

Once the smallest debt is paid:

Take its total payment and apply it to the next debt.

Example:

- First debt payment = $75

- Next debt minimum = $50

New payment = $125/month

Your payoff speed increases without increasing your budget.

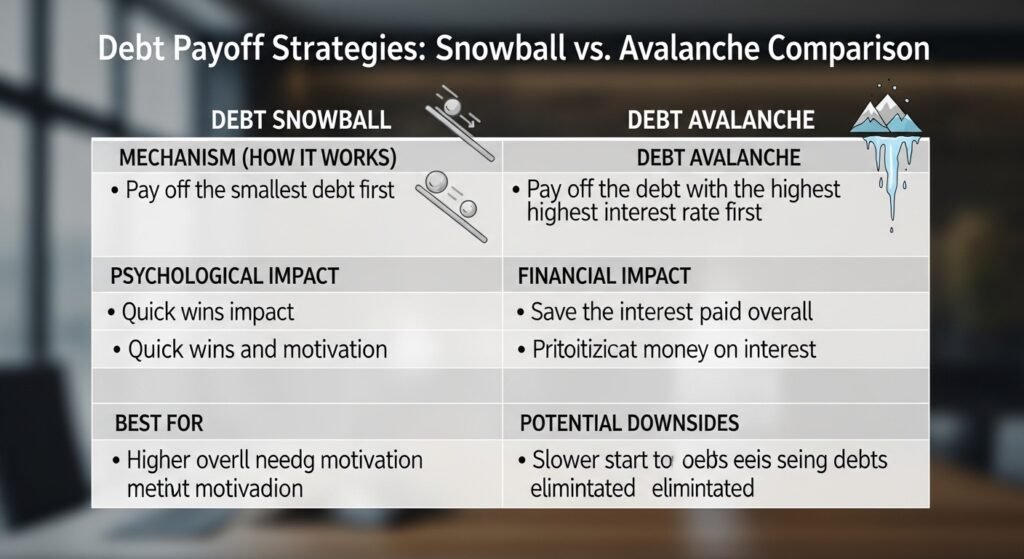

Debt Snowball vs Debt Avalanche (Fintech Comparison)

| Feature | Debt Snowball | Debt Avalanche |

|---|---|---|

| Focus | Smallest balance first | Highest interest first |

| Motivation | High (quick wins) | Moderate |

| Interest savings | Lower | Higher |

| Best for | Behavior change | Math optimization |

| Fintech automation | Easy | Easy |

For most users, snowball works better psychologically, especially when paired with visual fintech dashboards.

Best Fintech Features for Debt Snowball Plans

Look for apps that offer:

✔ Automated balance syncing

✔ Custom debt payoff ordering

✔ AI spending insights

✔ Bill reminders

✔ Goal-based budgeting

✔ Cash flow forecasting

Advanced tools now show:

- “Debt-free date” projections

- Interest saved over time

- Recommended extra payment amounts

Practical Tips to Accelerate Your Debt Snowball

Use Round-Up Savings for Extra Payments

Many fintech apps round purchases to the nearest dollar and send the difference to savings — redirect this to debt.

Redirect Windfalls

Apply to your smallest debt:

✔ Tax refunds

✔ Freelance income

✔ Bonuses

Cancel Unused Subscriptions

AI tools often detect recurring charges you forgot about.

Create a Debt Payoff Category in Your Budget

Treat extra payments as a fixed monthly bill.

Track Your Net Worth

Watching debt shrink while net worth rises increases motivation.

Common Debt Snowball Mistakes

❌ Skipping minimum payments

❌ Adding new debt during payoff

❌ Not tracking interest

❌ Ignoring due dates

❌ Quitting after the first debt

Consistency is the key to success.

Example: Fintech Debt Snowball Timeline

Starting debt:

- $300

- $600

- $2,000

- $4,500

Extra payment: $150/month

Estimated payoff:

✔ First debt: 2 months

✔ Second debt: 4 months

✔ Third debt: 10 months

✔ Final debt: 18 months

Total debt-free timeline: ~24 months

Without snowball momentum, it could take 3–4 years.

FAQs

Is the debt snowball method effective?

Yes. It’s proven to improve consistency and motivation, helping users pay off debt faster.

Can fintech apps automate a debt snowball?

They can automate minimum payments, track balances, and show payoff projections, but you direct extra payments.

Should I use snowball or avalanche?

Snowball for motivation and habit building; avalanche for maximum interest savings.

How much extra should I pay monthly?

Even $50–$100 extra significantly reduces payoff time.

Does debt snowball improve credit score?

Yes. Paying off balances and reducing utilization improves your score over time.

Advanced Strategy: AI-Powered Debt Optimization

In 2026, some fintech platforms offer:

✔ Predictive payoff timelines

✔ Smart payment allocation suggestions

✔ Cash flow alerts before due dates

✔ Automated debt prioritization

This combines behavioral psychology + machine learning for faster results.

Your Debt Snowball Action Plan

Here’s your step-by-step system:

- List all debts in a fintech app

- Sort by smallest balance

- Automate minimum payments

- Allocate extra monthly amount

- Track visual progress

- Roll payments forward

- Apply windfalls to smallest debt

Follow this consistently and you’ll build unstoppable momentum.

Final Thoughts: Turn Fintech Into Your Debt-Free Engine

The debt snowball method works because it:

✔ Builds confidence

✔ Creates visible wins

✔ Reinforces financial discipline

Fintech apps make it:

✔ Automated

✔ Data-driven

✔ Motivational

✔ Faster

You don’t need a higher income to become debt-free — you need a system.

Start today:

- Download a budgeting app

- Enter your debts

- Set your extra payment

- Pay off your first balance

Your first $0 balance is the moment your financial transformation begins.

✨ About Artisan Anthology

At Artisan Anthology, we curate timeless digital creations designed to inspire and elevate every part of your lifestyle. Our collection includes brand books, digital templates, recipes, ebooks, wardrobe planners, fashion guides, printable wall art, and elegant home décor designs. We also specialize in wedding cards, invitations, baby shower cards, and engagement cards, each crafted to celebrate life’s most meaningful moments.

For professionals and dreamers alike, our CV templates, guided journals, and manifestation planners are created with intention to help you tell your story beautifully and authentically.

✨ Discover our full collection of digital products here → ArtisanAnthology.xyz